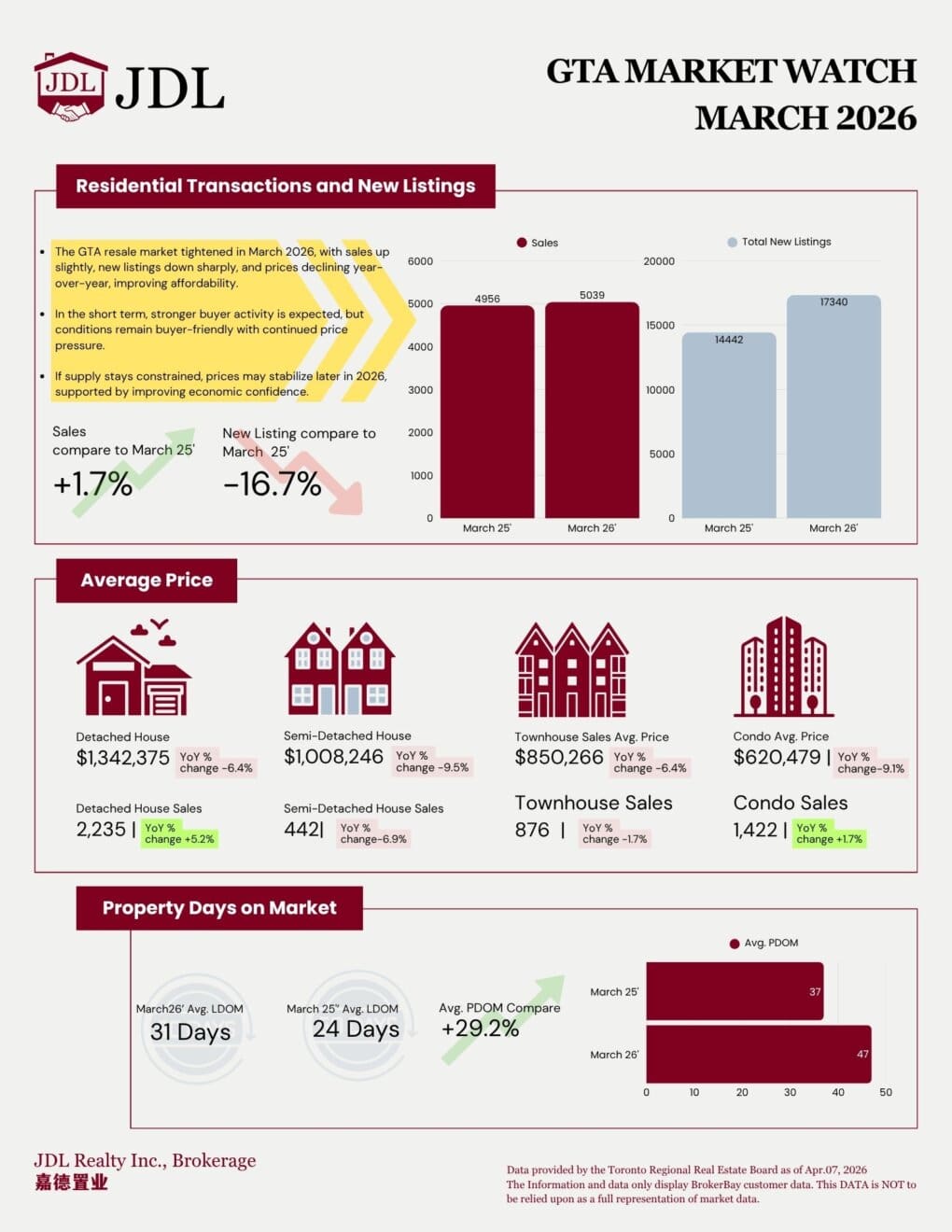

The GTA real estate market in March 2026 is entering a transitional phase.

Sales activity has shown early signs of recovery, while new listings have declined significantly, and prices remain in an adjustment cycle. These combined factors are reshaping market dynamics and gradually shifting the balance between buyers and sellers.

Sales Activity and Listing Trends

In March 2026, total residential sales reached 5,039 transactions, representing a +1.7% increase compared to March 2025.

At the same time, new listings declined sharply to 14,442 units, a -16.7% decrease year-over-year, indicating tightening supply in the resale market.

This combination of stabilizing demand and reduced inventory is beginning to increase competitive pressure, although overall conditions remain relatively balanced.

Market Context and Trend Analysis

The GTA resale market is currently characterized by a structural shift defined by rising transactions, declining supply, and price adjustments.

According to Toronto Regional Real Estate Board (TRREB) data, the decrease in listings alongside modest sales growth reflects a market that is gradually tightening after a period of correction.

From a pricing perspective, the market remains in transition. The MLS Home Price Index declined approximately 7.4% year-over-year, while the average selling price was about $1.017 million, down 6.7% compared to last year.

However, on a month-over-month basis, pricing trends have started to stabilize, suggesting that the market may be approaching a bottoming phase.

At present, buyers continue to hold relatively strong negotiating power, particularly in the condominium segment and certain move-up property categories.

Average Prices by Property Type

Price adjustments are evident across all major housing types:

Detached Homes: $1,342,375 (-6.4% YoY)

Semi-Detached Homes: $1,008,246 (-9.5% YoY)

Townhouses: $850,266 (-6.4% YoY)

Condos: $620,479 (-9.1% YoY)

While prices have softened compared to last year, this trend is contributing to improved affordability and increased accessibility for buyers.

Sales Performance by Property Type

Transaction trends varied across different housing segments:

Detached home sales: 2,235 (+5.2%)

Semi-detached home sales: 442 (-6.9%)

Townhouse sales: 876 (-1.7%)

Condo sales: 1,422 (+1.7%)

Detached homes and condos showed relatively stronger activity, while semi-detached and townhouse segments experienced slight declines.

Days on Market: A Key Indicator

Market liquidity has shifted, as reflected in longer selling timelines:

Average LDOM increased from 24 days to 31 days

Average PDOM increased from 37 days to 47 days, representing a +29.2% increase

This indicates that buyers are taking more time to evaluate options, and sellers may need to adjust expectations regarding pricing strategy and time on market.

What This Means for Buyers

For buyers, current conditions present a more favourable environment compared to previous years.

Lower prices, increased negotiation power, and longer decision timelines provide opportunities to enter the market with less pressure.

Although listing inventory has decreased, overall conditions still support a more balanced and accessible buying experience.

What This Means for Sellers

For sellers, strategy has become increasingly important.

Accurate pricing, strong marketing, and proper property positioning are essential to attracting serious buyers.

With longer days on market and more selective buyer behaviour, sellers must adapt to a more competitive environment.

Market Outlook

Looking ahead, market conditions are expected to gradually stabilize.

As the spring market progresses and supportive policies such as HST rebates and development charge adjustments take effect, buyer confidence may improve.

If listing inventory remains constrained while sales continue to recover, supply-demand conditions could move toward balance, potentially leading to price stabilization in the second half of 2026.

Long-Term Perspective

From a broader perspective, the GTA continues to face structural supply challenges, particularly in the “missing middle” housing segment—properties positioned between condominiums and detached homes.

If new housing supply does not keep pace with demand, the market may eventually return to a supply-constrained cycle, placing upward pressure on prices over the long term.

Final Thoughts

The GTA real estate market in March 2026 reflects a period of adjustment rather than decline.

With rising sales, reduced listings, stabilizing prices, and longer selling timelines, the market is transitioning toward a more balanced state.

Understanding these evolving conditions is essential for both buyers and sellers to make informed decisions in today’s real estate environment.

Source: Toronto Regional Real Estate Board (TRREB)

Your Industry Experts

We’re here to help. Whether you’re an agent or a client, we have the support and expertise you need to thrive in your next endeavour.